Blogs

Why API Integration of Video KYC is a Game-Changer for Policy Issuance

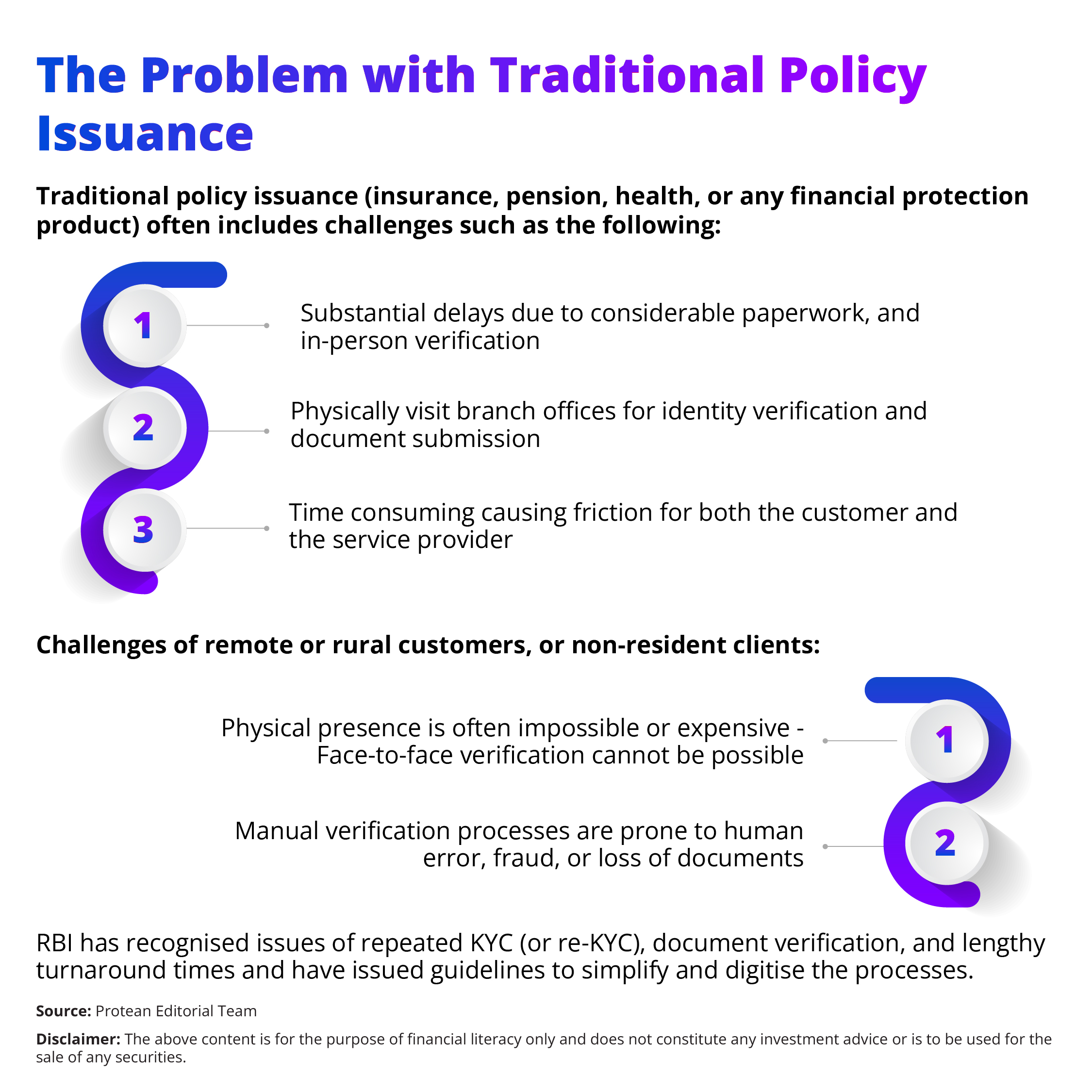

Video KYC API integration can be a boon in policy issuance.

Regulatory bodies like the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI) and GoI departments are pushing reforms that can simplify KYC norms and support digital modes of identity verification.

Recent amendments such as the RBI’s KYC (Amendment) Directions 2025 have explicitly added video-based customer identification processes (V-CIP) as a valid mode of onboarding customers. In this context, integrating video KYC through an API into policy issuance systems can be revolutionary.

What is Video KYC? A Quick Refresher

Video KYC, also known as Video-based Customer Identification Process (V-CIP) in India, is a digital identity verification method using live video calls. The process can involve a real-time audio-visual interaction between the customer and an authorised official of a regulated entity (RE), during which identity documents are shown, facial recognition and liveness checks are done, and customer due diligence is completed. The process is consent-based and governed under regulatory guidelines.

Under the recent RBI reforms, video KYC is now one of the permitted modes of onboarding customers, along with face-to-face and Aadhaar-OTP based e-KYC.

The rules also allow video KYC for reactivation of inoperative bank accounts or unclaimed deposits, making the process more accessible.

Why API Integration is a Must

API (Application Programming Interface) integration of video KYC means embedding video KYC functionality directly into policy issuance platforms, mobile apps, or web portals, allowing the video verification, document upload, facial matching, and regulatory checks to happen as part of the policy issuance workflow, without redirecting to external tools or manual handoffs.

Here are several reasons why this integration is essential:

- Speed and Efficiency – Automates the KYC process during policy application, cutting issuance time from days to minutes.

- Consistency and Compliance – Ensures every step meets RBI/IRDAI rules with liveness checks, secure storage, audit trails, and timestamps.

- Cost Reduction – Saves on branches, travel, staff, and paperwork by automating checks with Aadhaar, CKYC, etc.

- Scalability and Reach – Handles large customer volumes, across geographies and NRIs, unlike physical branches.

- Better Customer Experience – Enables smooth, digital onboarding from home with faster approvals.

- Regulatory Alignment and Risk Control – Keeps firms updated with RBI’s latest KYC norms, reduces compliance risks, and supports universal KYC or risk-graded eKYC.

Benefits of Video KYC API Integration

Below are concrete benefits that policy issuers (insurers, pension providers, mutual funds and similar regulated entities) gain:

- Faster policy issuance: Time from application to active policy drops significantly.

- Lower transaction costs: Savings in manpower, paper, office premises and logistics.

- Higher reach and inclusion: Remote applicants, rural customers, and those without easy access to branches can complete KYC and purchase policies.

- Improved security and anti-fraud measures: Liveness checks, face match, audio-visual record, document verification in real-time reduce impersonation or document forgery risk.

- Regulatory advantages: Being compliant with RBI’s V-CIP guidelines, SEBI or IRDAI norms, reduces legal risk and improves market reputation.

- Better customer retention and satisfaction: A smooth digital process reduces drop-outs, improves trust, reduces complaints.

Integration Process: A High-Level Overview for a Business

Here is a simple, step-by-step process businesses can follow to integrate video KYC via API into their policy issuance system:

- Requirements and Compliance Review

- Check RBI V-CIP, IRDAI VBIP, data storage, liveness detection rules.

- Align with internal legal, policy, and IT security standards.

- Choose API Provider or Build In-House

- Decide: partner with a vendor or develop internally.

- Look for features: video streaming, facial recognition, document upload, encryption, audit logs.

- API Design and Integration

- Set up API endpoints for user registration, document upload, video session start/finish, and verification.

- Integrate smoothly with mobile/web front-end.

- User Experience (UX) Flow

- Create simple screens for document capture and live video calls.

- Provide clear guidance and fallback if the connection fails.

- Ensure smooth liveness and face match checks.

- Security, Storage and Data Governance

- Store all video/data securely within India.

- Use encryption, timestamp logs, and retention/deletion policies.

- Ensure third-party vendors cannot misuse data.

- Testing and Pilot

- Run internal tests with a small group.

- Check compliance, user experience, video quality, and document accuracy.

- Full Roll-out and Monitoring

- Launch for all customers.

- Track metrics: policy issuance time, drop-off rates, fraud incidents.

- Conduct audits, ensure regulatory reporting, and use analytics to improve.

Conclusion

Video KYC, when properly integrated via APIs, transforms policy issuance in insurance, pensions and financial services. This model can offer a competitive edge by reducing time, cost and friction, and increasing reach and security. For any financial institution, adopting video KYC API integration is not just a tech upgrade, but a strategic necessity in a rapidly digitising market. Get in touch with Protean eGov’s team now for further information.

Frequently Asked Questions (FAQs)

- Is video KYC equal to face-to-face verification in India?

Yes. RBI treats Video KYC (V-CIP) as equal to in-person KYC if all rules like liveness, authorised officials, and document checks are followed. - Can video KYC be used for all policies?

Mostly yes. It works for most insurance and financial policies, but IRDAI may need extra checks for high-value or high-risk policies. - What if the video call drops?

The session must be restarted or resumed so all checks are properly captured. APIs should handle retries or fallback options. - How does cost compare with traditional KYC?

Once technology is set up, video KYC is cheaper, fewer branch visits, less staff, and lower paperwork costs. - Is data storage and privacy an issue?

Yes. All video and images must be encrypted, stored in India, with audit logs and access control. Customer consent, retention, and deletion rules must also be followed.

Related Articles