Blogs

Know when to shift your NPS Account from Corporate to Individual

Want to shift your NPS account from corporate to individual? You have come to the right article.

The National Pension System (NPS) is a government-regulated, market-linked retirement savings scheme that enables individuals to build a corpus for their post-retirement years.

Individuals who originally enrolled in NPS through their employer under the NPS Corporate Sector Model may face challenges in continuing their investments if they change jobs or exit the formal workforce.

In such scenarios, shifting from a Corporate NPS to an Individual NPS account (All Citizens Model) ensures continuity, personal control, and long-term stability in retirement planning.

What are NPS Account Types

The NPS has offered the following two main models to cater to diverse subscriber categories:

- Corporate NPS Account: This model allows employers to register with the NPS and offer it as a retirement benefit to their employees. Contributions can be made by both employer and employee. It provides convenience and may include organisational support in managing contributions and documentation.

- Individual NPS Account (All Citizens Model): Open to any Indian citizen aged 18–70 years, this model enables individuals to enroll and manage their NPS independently, without requiring an employer.

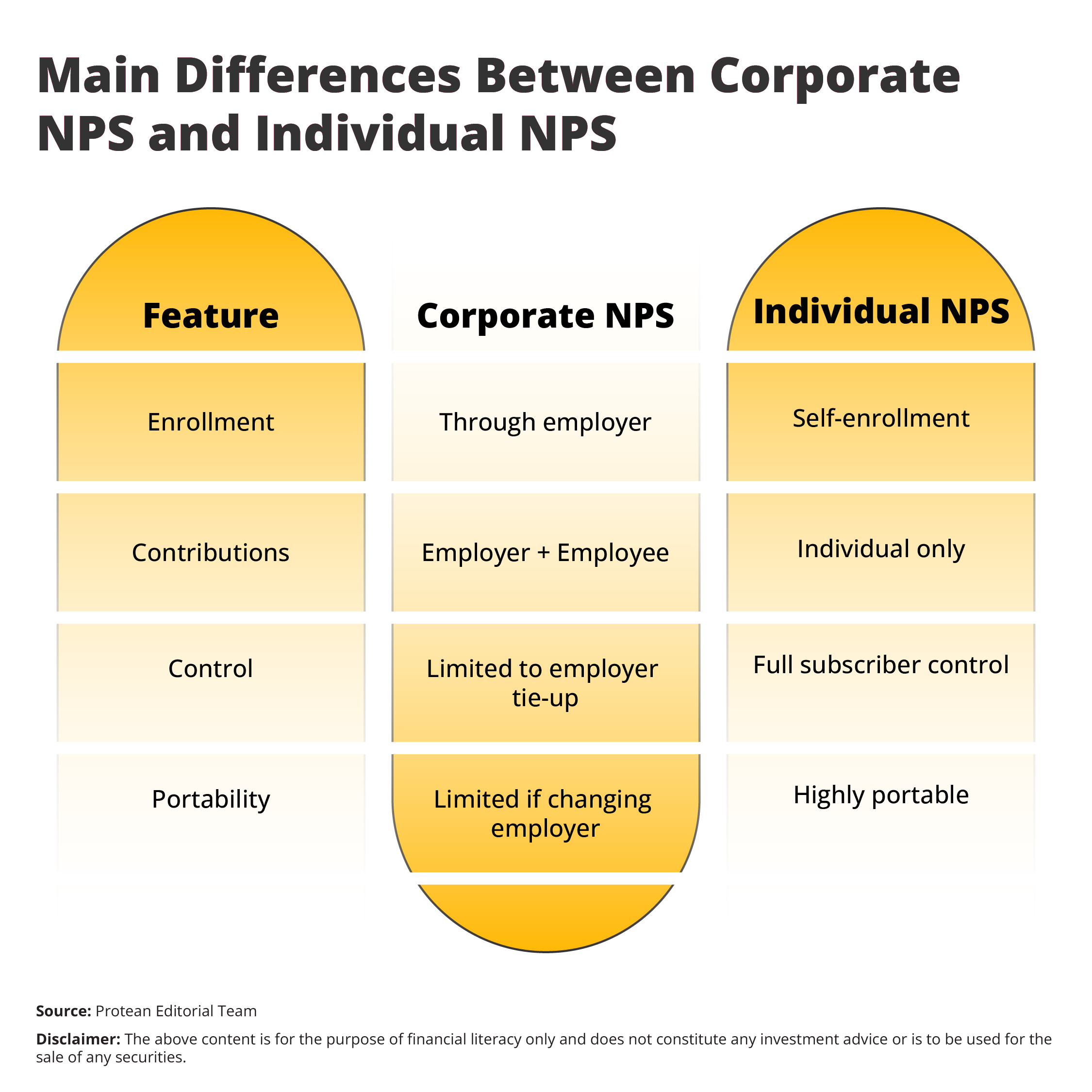

Main Differences Between Corporate NPS and Individual NPS

- The Corporate model offers ease of deduction from salary.

- The Individual model provides greater flexibility and portability, especially useful during job transitions.

When and Why to Shift from Corporate to Individual NPS

Shifting your NPS account from a Corporate model to the Individual model may become necessary under the following circumstances:

- Change of Job: If your new employer is not registered under the NPS Corporate model, contributions may stop.

- Leaving Employment: If you start a business, take a sabbatical, or retire early, your Corporate NPS account might become inactive unless migrated (Technically, the account does not become “inactive” immediately but will not receive contributions until migrated or otherwise funded).

- Need for Greater Control: Independent professionals and investors may want full control over their contributions, fund managers, and asset allocation.

- Tax Benefits: NPS contributions provide tax benefits under both the regimes.

Benefits of Shifting to Individual NPS Account

The benefits of shifting to individual NPS account can include the following:

- PRAN Continuity: Your existing Permanent Retirement Account Number (PRAN) remains unchanged.

- No Break in Investment: Contributions can continue seamlessly without employer involvement.

- Flexible Fund Management: You can gain the freedom to switch fund managers, change investment choices (Active vs Auto), and adjust equity-debt allocation per your risk appetite.

Transitioning to an Individual NPS account ensures that your retirement plan stays on track, regardless of employment changes.

Prerequisites for Shifting Your NPS Account

Before initiating the shift from a Corporate to Individual NPS model, you can ensure the following:

- Your PRAN is Active: Your Permanent Retirement Account Number must be operational with no outstanding issues.

- KYC Documents Are Ready: Keep a self-attested copy of your PAN, Aadhaar, and a recent photograph.

- Bank Account Details: You will need an active savings bank account with IFSC code for contributions and withdrawals.

- Employer Status Check: Verify whether your current or former employer is still registered with the Corporate NPS model.

- Mobile Number and Email: Ensure that your mobile number and email ID registered with the CRA (Central Recordkeeping Agency) are active for OTP and communication.

What are the Tax Benefits in Corporate NPS Account

The Corporate National Pension System (NPS) is an effective retirement planning tool that combines tax efficiency with long-term financial security for employees across various organisations.

This benefit is available to salaried employees working in organizations that are registered under the Corporate NPS model through a Central Recordkeeping Agency (CRA), such as Protean eGov Technologies Ltd. To extend this facility, the employer must hold a valid Corporate Registration Number (CRN), indicating a formal agreement with the CRA to offer NPS benefits to its employees.

The Corporate NPS model is accessible to both private and public sector organizations, offering flexibility for a wide range of employers to adopt this structured retirement solution. Employees eligible under this model must be Indian citizens or Non-Resident Indians (NRIs) and fall within the age bracket of 18 to 70 years.

As part of the scheme, private sector employers can contribute up to 10% of the employee’s salary (Basic + Dearness Allowance), while central government employers may contribute up to 14%. These contributions are eligible for exclusive tax deductions under Section 80CCD(2) of the Income Tax Act and are available over and above the standard ₹1.5 lakh deduction under Section 80C.

What are the Tax Benefits in Individual NPS Account

As outlined earlier, the Individual NPS Account offers multiple advantages, and its tax benefits are a key aspect worth noting. The Individual NPS is a voluntary retirement savings scheme available to all Indian citizens and NRIs aged 18 to 70 years, with no employer involvement required. It is particularly suitable for self-employed professionals, business owners, freelancers, and salaried individuals and others who wish to take charge of their own retirement planning.

Its Main Tax Benefits are:

- Deduction of up to ₹1.5 lakh under Section 80CCD(1), included within the overall Section 80C limit.

- An additional deduction of ₹50,000 under Section 80CCD(1B), over and above the Section 80C ceiling.

The Individual NPS thus offers a flexible and tax-efficient framework for building long-term financial security independently.

Conclusion

Switching from a Corporate to an Individual NPS account can be a prudent step for ensuring uninterrupted retirement planning, especially during job transitions or employment breaks. It can allow you to retain control over your investment choices and maintain the same PRAN without disruption. With digital platforms enabling a seamless shift process, subscribers should not delay this important transition. Keeping your documents ready, understanding the process, and acting in time can ensure your NPS account continues to grow without interruption, paving the way for a secure and well-planned retirement.

Frequently Asked Questions

Q1: What if my employer delays the process?

The NPS account shift can be initiated by the subscriber directly via the CRA portal without employer involvement.

Q2: How long does the shift take?

Typically, 5–10 working days are required for NPS account shift post successful submission and document verification.

Q3: What happens to my existing NPS balance?

Your entire corpus, fund allocation, and PRAN remain intact. Only the subscriber sector changes, from Corporate to Individual.

Related Articles