Blogs

NPS Tax Benefits: A Breakdown of Every NPS Deduction Section for Taxpayers

Have you made your NPS contribution this year? Before investing in NPS in 2025, you might want to refresh your knowledge on NPS tax benefits and NPS deduction section details.

The National Pension System (NPS) is a structured avenue for retirement planning in India. It also offers NPS tax benefits. However, taxpayers might face ambiguity in distinguishing the three NPS deduction sections and their applicability under the old and new tax regimes.

Let us clearly analyse each NPS deduction section, along with recent developments. Let us look at the enhanced employer contribution limit for private and public sector employees under the new regime and the introduction of the Systematic Lump Sum Withdrawal (SLW) facility at exit.

What is NPS? Dissecting the NPS Scheme

National Pension System (NPS) is PFRDA regulated, market-linked, and cost-effective retirement scheme.

Under NPS, investors can do the following:

- Open a Tier I account, designed for building a retirement corpus with defined withdrawal rules

- Open a Tier II account (optional), which functions as a flexible savings facility without tax benefits.

Contributions are allocated across equity, corporate bonds, government securities, or a life-cycle portfolio, depending on the subscriber’s preference.

At the retirement age of 60 years, up to 60% of the accumulated corpus may be withdrawn tax-free as a lump sum. Here, a minimum of 40% is mandatorily invested in an annuity, with the resulting income taxed in the year of receipt.

Additionally, partial withdrawals of up to 25% of self-contributions, permitted for specified purposes, are exempt from tax.

Together, these provisions give NPS an EEE-like treatment at exit for the lump sum portion.

Breaking Down the Main NPS Deduction Sections

Let us learn more about NPS deduction sections:

1) The Foundation: Section 80CCD (1)

Section 80CCD (1) can apply to an individual’s own contribution to NPS.

This NPS tax benefit is available only under the old tax regime.

- It’s included within the overall limit of ₹1.5 lakh under Section 80CCE.

- This section can also cover Section 80C and Section 80CCC.

- The new tax regime does not permit this deduction.

The comparison is as follows:

Old Regime

- Private & State Government Employees: Deduction up to 10% of salary (basic + DA).

- Central Government Employees: Higher limit of 14% of salary (basic + DA).

- Self-Employed: Deduction up to 20% of gross total income, capped at ₹1.5 lakh.

New Regime

- No deduction available under Section 80CCD (1).

- Only employer contributions under Section 80CCD (2) qualify.

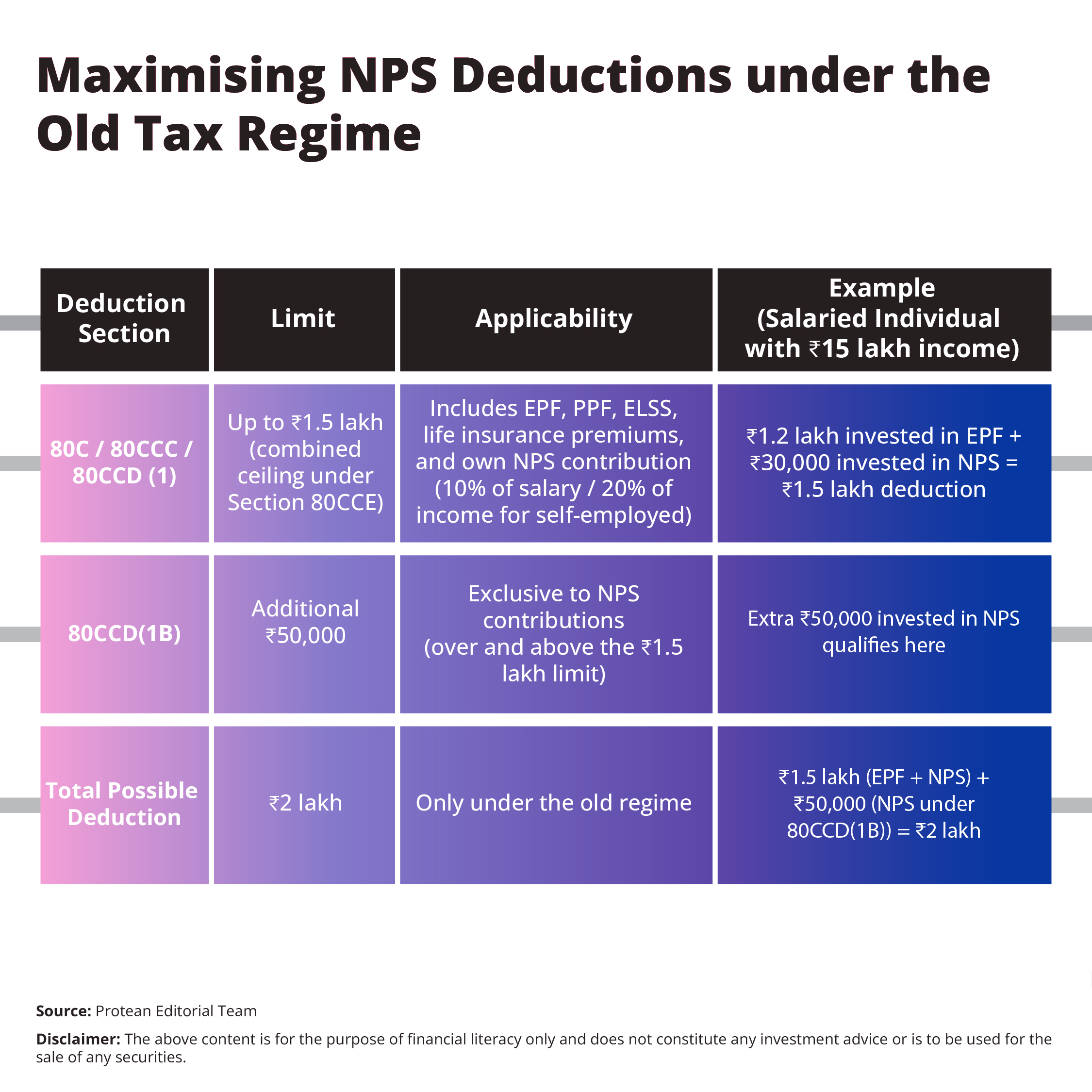

2) The Additional Benefit: Section 80CCD(1B)

Under the old tax regime only, Section 80CCD(1B) can provide an additional NPS deduction of up to ₹50,000 over and above the ₹1.5 lakh ceiling of 80C/80CCC/80CCD(1).

Let us understand this with the help of this example:

Maximising NPS Deductions under the Old Tax Regime

3) The Employer’s Contribution: Section 80CCD (2)

- It can cover employer contributions to the employee’s NPS Tier I account.

- Available under both old and new regimes, making it valuable when other deductions are disallowed in the new regime.

Budget 2024 update - Enhanced NPS Benefits:

- For private and PSU employees, the limit has been raised from 10% to 14% of salary (basic + DA) under the new regime.

- Central Government employees already enjoyed the 14% limit.

- Overall ceiling: Employer contributions to EPF + NPS + Superannuation Fund are tax-free only up to ₹7.5 lakh per year. Excess is taxable along with accretions.

Tax Benefits on Returns and Withdrawal

NPS can help you make tax-efficient accumulation and preferential exit.

Let us understand with the help of the following:

- Exit at 60: Up to 60% of the corpus can be withdrawn tax-free; at least 40% must buy an annuity, and annuity income is taxable as per your slab.

- Systematic Lump Sum Withdrawal (SLW): It allows tax-free 60% into periodic payouts (monthly/quarterly/annual) until age 75 years. It smoothens the cash flows, though clarity on tax treatment of growth during SLW is awaited.

- Partial withdrawals: Up to 25% of self-contributions are tax-free, adding flexibility for conditional withdrawals.

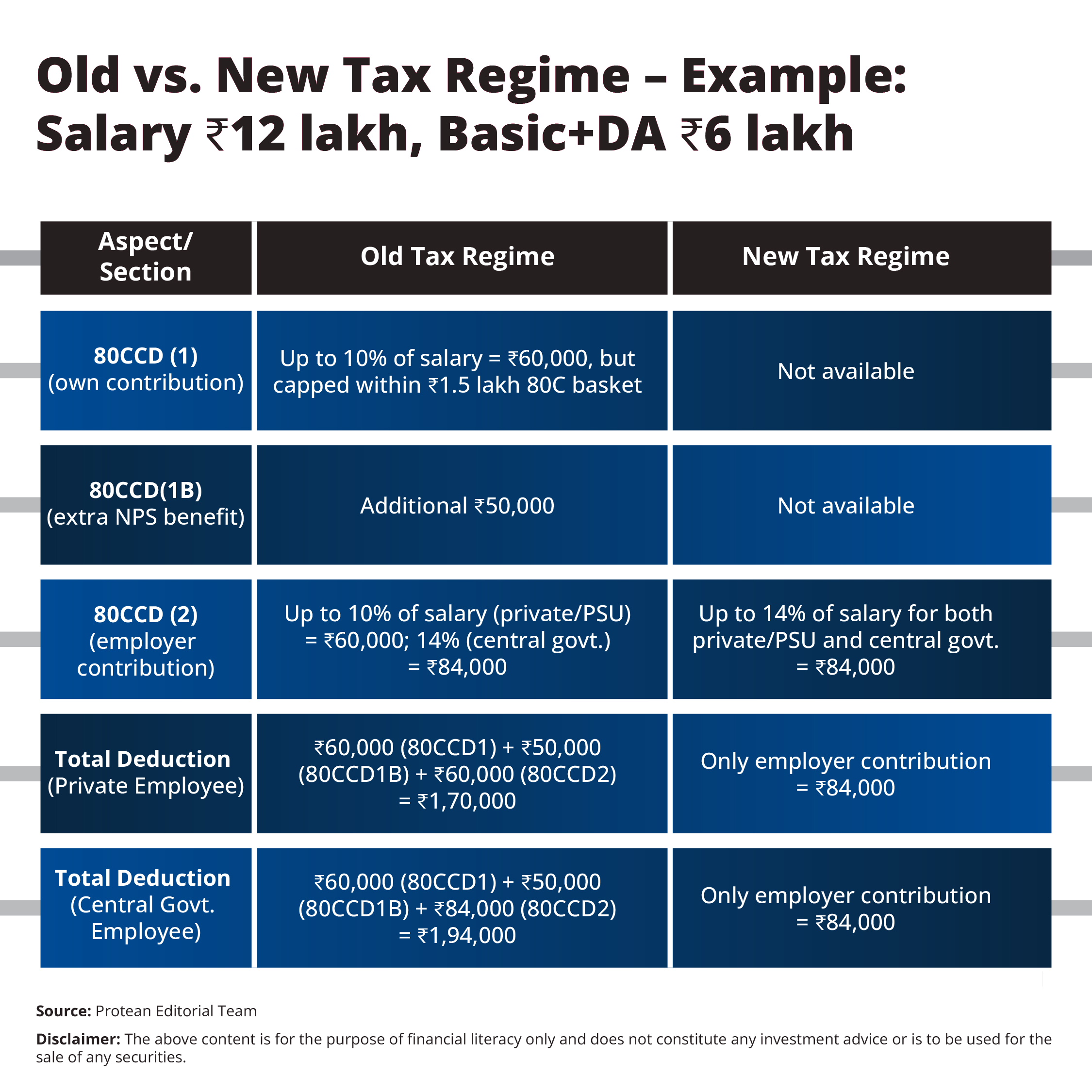

Old vs. New Tax Regime – Example: Salary ₹12 lakh, Basic+DA ₹6 lakh

Here are some of the main observations on NPS deduction section and NPS tax benefits:

- The old regime gives higher deductions (up to ₹2 lakh) if you actively contribute.

- The new regime is leaner, but 80CCD (2) employer contribution remains a strong benefit, especially with the new 14% parity for private/PSU employees.

Conclusion

The National Pension System (NPS) has provided well-defined tax benefits that can encourage long-term retirement planning. Under the old tax regime, individuals can claim deductions through Section 80CCD(1) within the ₹1.5 lakh ceiling and an additional ₹50,000 under Section 80CCD(1B).

Beyond personal contributions, both the old and new regimes allow deductions under Section 80CCD(2) for employer contributions. Following recent changes, this limit has been increased to 14% of salary for private and PSU employees, aligning them with central government employees.

Since the new regime does not permit personal deductions, Section 80CCD(2) now stands out as the primary tax-saving opportunity for NPS subscribers.

Frequently Asked Questions

Q1: Can self-employed individuals claim NPS tax benefits?

Yes. They can claim up to 20% of gross total income under 80CCD (1) within the ₹1.5 lakh 80C ceiling, plus ₹50,000 under 80CCD(1B) in the old regime.

Q2: Are Tier II contributions eligible for NPS tax deductions?

No. Tier II has no deduction benefits. Tax breaks apply to Tier I.

Q3: Which NPS deduction is allowed in the new tax regime?

80CCD (2) for employer contributions; and for private/PSU employees under the new regime, the limit is 14% of salary after the latest change.

Q4: Is the 60% withdrawn at retirement always tax-free?

Yes, subject to NPS exit rules; annuity income is taxable. SLW lets you phase the tax-free 60% over time.

Related Articles