Blogs

NPS vs. Other Investments in the New Tax Regime

Are you curious about the NPS in new tax regime or the NPS tax benefits?

The new tax regime has aimed to simplify India's tax laws by offering lower tax rates.

However, there is a removal of most popular tax deductions that came with the old tax regime.

This might raise critical questions like:

- How does one save on taxes now?

- How does NPS in new tax regime work?

Here’s putting the National Pension System (NPS) into the spotlight with its unique and powerful tax advantage.

Understanding the NPS in New Tax Regime

The new tax regime is now the default option for taxpayers. It has eliminated over 70 tax exemptions and deductions.

These eliminated ones include the widely used:

- Section 80C (for PPF, ELSS, life insurance)

- Section 80D (health insurance)

- HRA (House Rent allowance)

- Self-contribution to NPS under Sections 80CCD(1) and 80CCD(1B)

However, one crucial provision has survived.

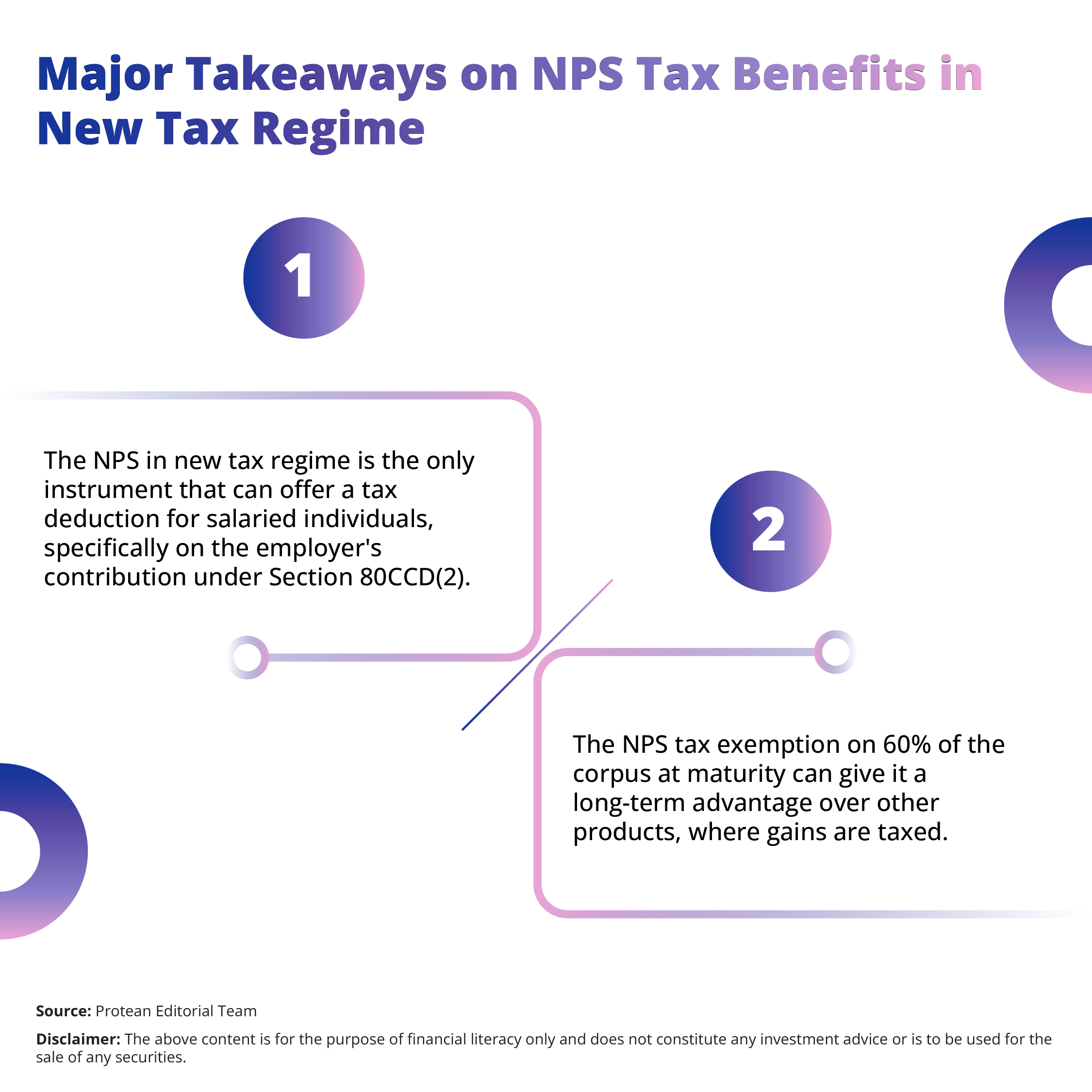

These are the NPS tax benefits under Section 80CCD(2). This section can allow for a tax deduction on the employer's contribution to an employee's NPS Tier-I account. This can make the NPS in new tax regime a uniquely valuable instrument for salaried individuals. NPS can offer a tax-saving avenue that other investments no longer provide.

NPS vs. Other Key Investments

Let us check how the NPS in new tax regime can compare against other popular financial products.

NPS Tax Benefits - Corporate Model

The employer's contribution of up to 10% of the employee's basic salary plus dearness allowance is deductible from taxable income under Section 80CCD(2).

- It’s a direct reduction of your tax liability.

- NPS tax exemption on maturity is a significant plus.

- Upon reaching 60, you can withdraw up to 60% of the corpus as a tax-free lump sum.

- The remaining 40% must be used to purchase an annuity, the income from which is taxed.

NPS (for salaried employees) can offer a rare deduction that can directly lower taxable income. It can also help in building a long-term retirement corpus.

The partial NPS tax exemption at maturity can add to its special features.

Public Provident Fund (PPF)

PPF was known for its Exempt-Exempt-Exempt (EEE) status.

- Interest earned and the maturity amount remain tax-free even under the new tax regime

- Deduction on contribution under Section 80C is gone in the new tax regime

PPF remains a safer, long-term debt instrument with tax-free returns. However, it can offer zero tax-saving benefits on the investment amount under the new rules.

Equity Linked Savings Scheme (ELSS)

Similar to PPF, ELSS funds have lost their tax-saving power on the investment side.

- Section 80C deduction is unavailable

- Long-term capital gains (LTCG) from ELSS exceeding ₹1 lakh (Rs. 1.25 lakhs from 23 July 2024 onwards) in a financial year are taxed at 10% (12.5% from 23 July 2024 onwards). Therefore, SIPs before and after 23 July 2024 would be taxed accordingly on redemption

ELSS can still provide the potential for high, equity-linked returns. However, from a pure tax-saving perspective, it can no longer offer an upfront advantage.

Tax-Saving Fixed Deposits (FDs)

FDs also fall under Section 80C. So, under the new tax regime:

- Deduction on the investment amount is no longer available.

- Interest earned on these FDs is fully taxable as per your income tax slab

FDs can offer no deduction, and the returns are taxed.

Unit Linked Insurance Plans (ULIPs)

The deduction for ULIP premiums under Section 80C is not available in the new regime. For policies issued after February 1, 2021, if the total annual premium exceeds ₹2.5 lakh, the maturity proceeds are also subject to tax.

Conclusion

While the new tax regime has simplified calculations by removing most deductions. It has effectively elevated the importance of the National Pension System for salaried taxpayers. It can be a tool that allows you to reduce your taxable income while systematically building a fund for your golden years. You leverage NPS tax benefits in your portfolio to ensure that your financial plan is both future-ready and tax-efficient.

Frequently Asked Questions

Q1: Is the self-contribution of ₹50,000 under Section 80CCD(1B) available in the new tax regime?

No. The additional deduction for self-contribution to NPS under Section 80CCD(1B) is not available if you opt for the new tax regime. The only available NPS tax benefit is on employer's contribution.

Q2: Is the entire maturity amount from NPS tax-free?

No, the full amount does not qualify for NPS tax exemption. You can withdraw up to 60% of the total corpus tax-free upon maturity (at age 60). The balance of 40% must be used to purchase an annuity plan, and the pension income received from that annuity is taxable as per your income slab.

Q3: As a self-employed individual, is there any reason to invest in NPS under the new tax regime?

NPS remains a very low-cost and professionally managed retirement savings product that can help you build a substantial corpus for your post-retirement life.

Q4: How can I avail the deduction for the employer's contribution to NPS?

NPS deduction can only be availed if your employer is a part of the corporate NPS model and this contribution is included in your CTC structure. You need to discuss this with your HR or finance department to opt-in and have them make contributions to your NPS account on your behalf.

Related Articles