Blogs

NPS Interest Rate: Why It Is Not a Fixed Rate and What to Check Instead

Are you seeking predictable or stable growth for your retirement corpus?

You do not need a fixed NPS interest rate to achieve this goal.

There is a fundamental misunderstanding of how the National Pension System operates.

There is no fixed NPS interest rate scheme available. NPS returns are market-linked. They are designed for long-term wealth creation, where returns are dynamic and variable.

Let us explore why a fixed NPS interest rate does not exist, explain how NPS returns are actually generated.

Let’s discuss the "NPS Interest Rate" ideology

The National Pension System (NPS) does not offer a pre-determined or fixed interest rate. Unlike instruments where the government or a bank guarantees a specific rate of return for a certain period, NPS investments are connected to the financial markets.

This means, the money you contribute is invested in a mix of assets. The value of these investments can fluctuate based on market performance.

Therefore, the gains or losses on your investment are not NPS interest rates in the traditional sense.

- The term NPS interest rate is a misnomer

- A more accurate term to use and track is NPS returns

- NPS returns are market-driven returns.

How NPS Returns Are Generated

It is important to understand the mechanism behind NPS returns to recoginse its potential.

Your contributions are not just sitting in a NPS account. They are actively invested by professional Pension Fund Managers (PFMs). As a subscriber, you have the flexibility to decide how their money gets allocated across different asset classes.

There are four primary asset classes at the core of NPS investment. Each of them come with their own risk and return profile:

- Asset Class E (Equity): This portion of your funds goes into the share market, investing in company shares. Equities can have the potential for high returns over the long term. However, they might also come with higher risk due to market volatility.

- Asset Class C (Corporate Bonds): Here, you invest in debt securities issued by private companies. These can be generally less risky than equities and can offer more stable, moderate returns.

- Asset Class G (Government Securities): Here, you invest your funds in bonds issued by the central and state governments. These might be considered as a safer investment class, offering lower but highly secure returns.

- Asset Class A (Alternative Investment Funds): Here, there is an investment basket of more complex instruments like Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), and other alternative funds. This option can carry a higher risk and can be better for more sophisticated and risk-loving investors.

The performance of these underlying assets can directly determine your NPS returns.

The value of your investment is tracked through the Net Asset Value (NAV).

- The NAV represents the market value of one unit of your NPS scheme.

- NAV changes daily, reflecting the performance of the assets in the fund's portfolio.

- When you contribute, you buy units at the prevailing NAV.

- As the value of the assets grows, the NAV increases, and so does the value of your investment.

What to Check Instead of a Fixed NPS Interest Rate

Since a fixed NPS interest rate is off the table, a savvy investor needs to know what metrics to monitor.

Thus, your focus needs to shift from searching for a fixed number to evaluating the factors that actively influence your fund's growth.

Here is what you can check instead:

Pension Fund Manager (PFM) Performance

There are multiple PFMs appointed by the PFRDA to manage NPS funds. These managers have different track records. You should regularly review the historical performance of various PFMs across all asset classes (E, C, and G) over different time horizons, such as 1-year, 5-year, and since inception.

A consistent, long-term performance record is a good indicator of a fund manager's capability.

Historical Scheme Returns

Instead of a single rate, look at the annualised returns generated by your specific NPS scheme.

The CRA portals (like Protean eGov technologies) provide detailed statements showing how your chosen scheme has performed over time. This data gives you a realistic picture of your investment's growth.

Your Asset Allocation

The mix of E, C, and G in your portfolio is the single biggest factor that determines your NPS returns. A higher allocation to equity (Asset Class E) offers the potential for higher returns but also higher risk.

You can periodically review your asset allocation to ensure it aligns with your risk appetite and retirement goals.

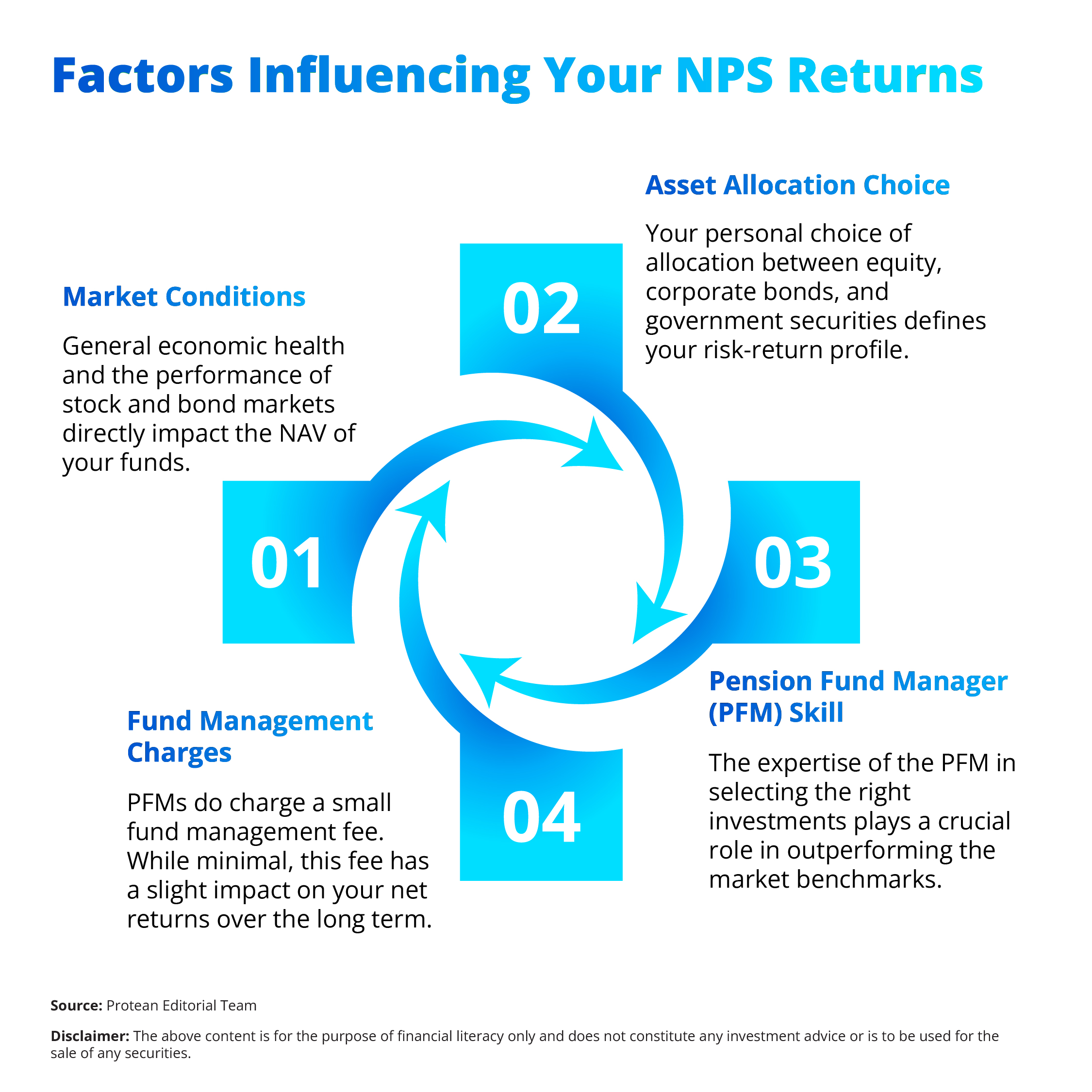

Factors Influencing Your NPS Returns

Your final retirement corpus can depend on a combination of factors that work together. Understanding these elements can empower you to make informed decisions about your investment strategy.

Conclusion

It is time to move past the search for a fixed NPS interest rate delusion and embrace the reality and potential of market-linked returns.

The National Pension System is designed not to provide fixed, modest gains but to build a strong retirement corpus through the power of compounding and long-term market growth.

Your role as an investor is to stay informed, choose your asset allocation wisely, and monitor the performance of your pension fund manager.

The variable nature of NPS returns is a feature, not a flaw, offering you the opportunity for wealth creation that fixed-income products often cannot match.

Frequently Asked Questions

Q1: Is there any part of NPS that offers a guaranteed interest rate?

No, NPS is a market-linked product, and returns are not guaranteed. The underlying assets, including government securities (Asset Class G), are subject to market risks. While Class G is the most secure, its returns still fluctuate based on bond market dynamics and are not fixed.

Q2: How frequently do NPS returns change?

The NPS returns change daily. The Net Asset Value (NAV) of each NPS scheme is calculated at the end of every business day based on the closing market prices of the assets in its portfolio.

Q3: Where can I track my NPS returns?

You can track the performance of your NPS account by logging into your account on the website of your Central Recordkeeping Agency (CRA), such as Protean eGov. You can also use the official NPS mobile app, which provides a detailed statement of your holdings and their current market value.

Related Articles