Blogs

How NPS scheme provides Inflation Protection and Long-Term Wealth Creation

What is the National Pension System (NPS)?

Can investing in an NPS scheme help in retirement planning and inflation management?

Let us find out!

Investing in the National Pension System can offer you a dual promise of:

- Long-term wealth creation

- Protection against inflation

An NPS scheme is backed by prudent fund management and regulatory oversight from the Pension Fund Regulatory and Development Authority (PFRDA).

Thus, the NPS scheme is popular among both salaried individuals and the self-employed as a retirement planning tool.

Let us learn more about the NPS scheme, NPS tax benefits and NPS returns

NPS for Long-Term Wealth Creation

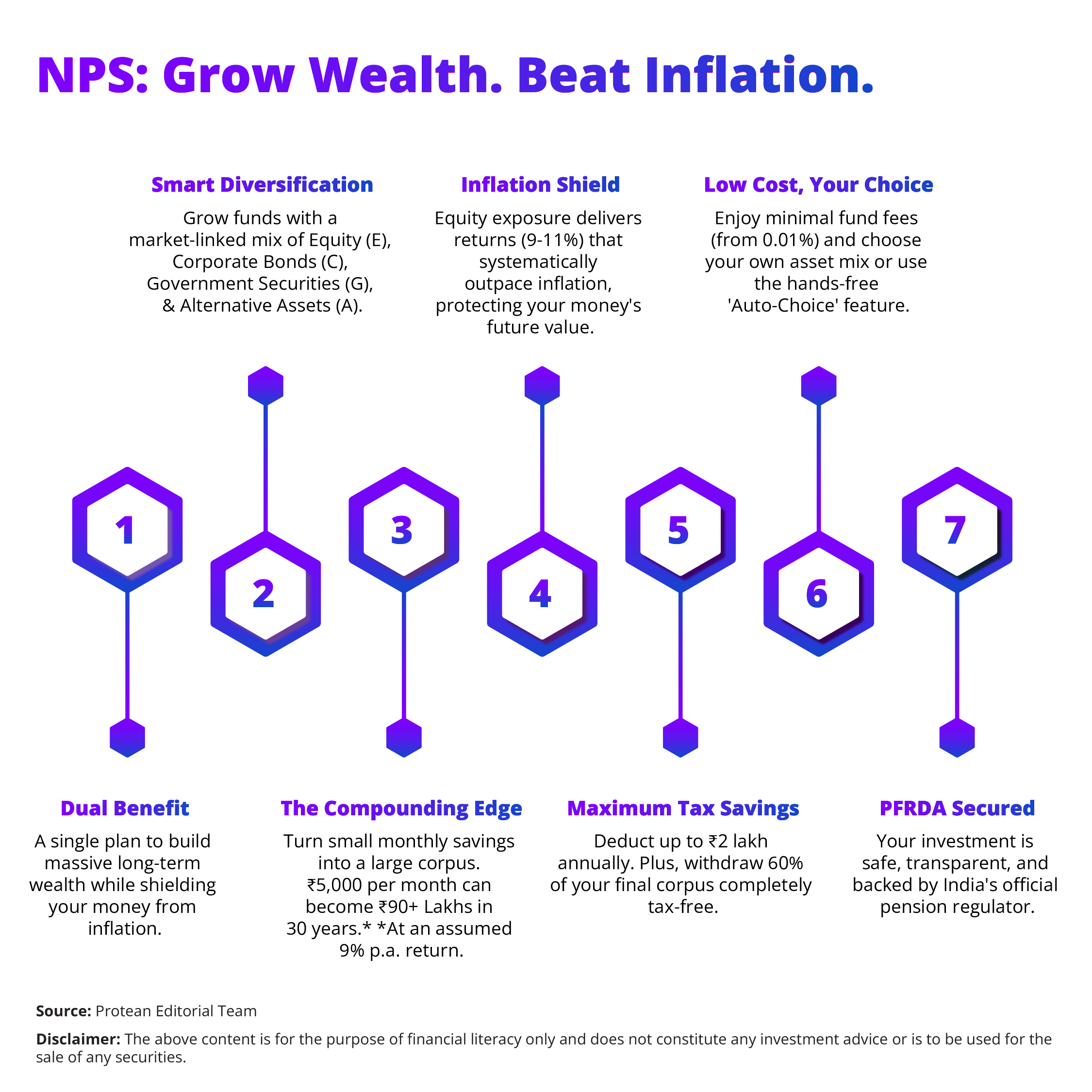

The NPS scheme has the ability to generate market-linked returns. This can set it apart from traditional pension products. Under NPS, contributions are allocated across a mix of:

- Equity (Asset Class E)

- Corporate bonds (C)

- Government securities (G)

- Alternative investments (A)

This diversified allocation can help optimise risk-adjusted returns over the long term.

| Also Read: Best Pension Plan in India |

The power of compounding in National Pension System investments can potentially enhance wealth creation. Compounding can generate higher potential returns with time. This can happen when investors contribute to an NPS scheme consistently from a young age.

Thus, even small monthly contributions, investors can accumulate into a strong retirement corpus, with several decades of National Pension System investing. For instance, assuming an average annual return of 9% over 30 years, a monthly investment of ₹5,000 can potentially grow to over ₹90 lakhs.

NPS scheme investments can also offer flexibility to choose asset allocation and fund managers or opt for the auto-choice lifecycle option. The auto choice option can automatically adjust the asset mix based on the subscriber’s age.

According to several reports, for equity schemes, the average annualised return since inception has been in the range of 9% to 11%, making NPS competitive with mutual funds.

NPS Investment and Inflation Protection

Inflation is one of the most pressing threats to post-retirement financial stability. Inflation can steadily erode your purchasing power of accumulated savings.

The National Pension System has investment options with exposure to equities and market-linked instruments. This can help you manage inflation and protect your long-term financial goals from it.

The higher potential returns from equity investments within an NPS scheme can help maintain the real value of savings. This can help especially when inflation averages between 5-6% per annum. Over longer investment horizons, equity performance typically outpaces inflation, allowing the retirement corpus to retain its purchasing strength.

| Also Read: How NPS can help you build a secure retirement |

There is also an evolving policy landscape aimed at enhancing inflation protection. For instance, the introduction of the Unified Pension Scheme (UPS), intends to integrate aspects of inflation-adjusted payouts, particularly for government employees. Further, experts have called for inflation-indexed annuity options, which can ensure that pension income rises in line with inflation post-retirement. However, the current design of the NPS scheme, with its growth-oriented investment strategy, can provide a solid foundation for mitigating inflation risk, particularly during the accumulation phase.

NPS Tax Benefits and Additional Advantages

There are tax benefits associated with the NPS scheme. In fact, the NPS scheme is one of the more tax-efficient retirement planning tools under the current Indian tax regime.

The National Pension System contributions qualify for deduction under Section 80C (within the overall ₹1.5 lakh limit), and an additional exclusive deduction of up to ₹50,000 under Section 80CCD(1B) is available effectively allowing a total tax benefit of up to ₹2 lakh per year.

At maturity, 60% of the corpus can be withdrawn tax-free, while 40% must be used to purchase an annuity, which is taxable as per the subscriber’s slab. NPS also boasts a low-cost structure, with annual fund management charges as low as 0.01%, significantly lower than mutual funds or ULIPs.

| Also Read: Plan your retirement with NPS |

Moreover, the PFRDA ensures robust regulatory safeguards, transparent NAV disclosures, and online access to account details. This has further strengthened its appeal to investors seeking both security and growth.

Conclusion

The National Pension System or NPS scheme has a wide range of investment options. These options can particularly be better for building a strong retirement corpus, NPS tax benefits and managing the impact of inflation on your long-term wealth creation goals. The NPS scheme can combine market-linked growth with a cost-efficient structure and favorable tax treatment. It can thus enable individuals to create long-term wealth with steady and regular investing.

The equity exposure of the National Pension System investments and potential policy advancements can make it a better investment option for safeguarding retirement savings against inflation.

As India moves toward a more pension-conscious society, the NPS scheme can play a pivotal role in ensuring financial independence during retirement for millions of individuals across diverse income segments.

Frequently Asked Questions

Q1: How does NPS help protect against inflation?

National Pension System or NPS scheme’s equity exposure and market-linked components can typically generate higher potential long-term returns, helping to offset inflation’s impact.

Q2: What kind of returns can I expect from NPS?

The NPS scheme returns can vary based on asset allocation and fund performance.

Q3: Are NPS withdrawals tax-free?

At maturity, 60% of the NPS scheme corpus is tax-free, and the remaining 40% must be used to buy an annuity, which is taxed as per your income slab.

Q4: Can I change fund managers or asset allocation?

Yes, the NPS scheme subscribers can switch fund managers twice a year and adjust asset allocation up to four times a year.

Q5: Is NPS suitable for self-employed individuals?

Absolutely. The NPS investment is open to all Indian citizens aged 18–70 years, including self-employed professionals who want to build a secure retirement corpus.

Related Articles