Blogs

The Role of CKYC in Seamless Bank Account Onboarding in India

Does the CKYC process simplify account opening and onboarding? Let’s find out:

Before the introduction of centralised systems, opening a bank account was a lengthy and document-heavy process. Customers had to go through lengthy processes where they had to:

- Provide several identity and address proofs

- Submit physical copies

- Repeat the same procedures each time they engage with a new financial institution.

For banks and other entities, this had created redundant verification tasks, increased operational costs, and prolonged onboarding timelines. The outcome was a poor customer experience, higher abandonment rates during account opening, and a fragmented understanding of customer identity across regulated institutions.

Thus there was a need for a more straightforward CKYC process. Here’s more about the CKYC India process and CKYC number.

The old way vs. the new way: Why CKYC number was needed

Traditionally, KYC (Know Your Customer) verification was a fragmented system. It led to duplicate records, inconsistent data, and significant compliance challenges.

To address these inefficiencies, the Central KYC (CKYC) framework was introduced. This CKYC process provided a unified and interoperable repository of verified KYC records. These records could be accessed by all regulated financial institutions.

Under this system, the customers need to complete KYC only once to obtain a unique CKYC number.

The CKYC number can then be quoted for future financial relationships. This centralised approach thus, eliminated duplication, saved time, and ensured uniform regulatory compliance across the financial ecosystem.

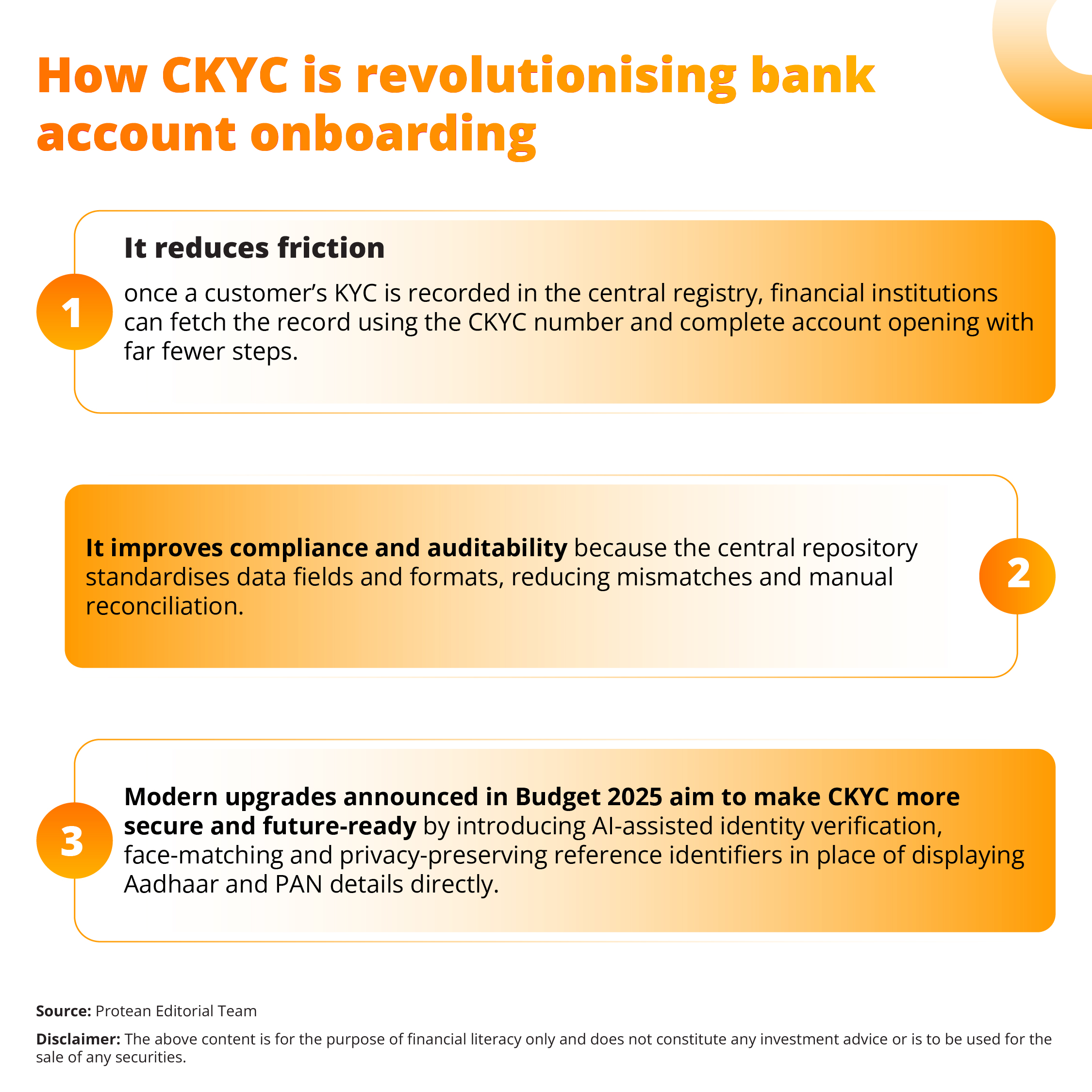

How CKYC is revolutionising bank account onboarding

CKYC is changing onboarding in the following three practical ways:

These changes are intended to:

- Cut onboarding times

- Reduce duplicate records

- Strengthen data privacy

The implementation of CKYC 2.0 entrusted to system integrators and technology partners, can further accelerate this transformation.

Various entities deliver the next-generation CKYC registry that can do the following:

- Modernise interfaces

- Introduce robust APIs for regulated entities

- Provide operational support for ongoing verification and updates.

Such investments can make routine KYC a background capability rather than a repeated customer task.

How CKYC works for the customer

From a customer’s perspective, CKYC is straightforward. Let us look at the CKYC India process:

- At the time of the first financial interaction (for example, opening a bank account or buying a fund), the customer submits standard identity and address documents.

- The submitting entity uploads the validated record to the central CKYC repository.

- The registry issues a unique CKYC number for that individual, which the customer or any regulated entity can quote in future transactions.

- The CKYC number therefore becomes the canonical pointer to the validated KYC dossier, sparing the customer from repeated submission of the same proofs.

This model can streamline onboarding and make product switching and multi-provider relationships far less burdensome.

The future of banking in CKYC India

The segment of CKYC in India deals with interoperability and smarter verification methods:

- Financial regulators target a universal KYC framework that would increase the inter-usability of CKYC records across sectors and reduce duplicate checks by banks, insurers and capital-market intermediaries.

- Parallel upgrades such as AI-driven de-duplication, biometric face-matching and use of consent-based reference IDs instead of exposing Aadhaar/PAN improve both speed and privacy of onboarding.

- For banks, this may lower operational cost per account and faster time-to-revenue for deposits and lending products.

- For customers, the future promises near-instant onboarding for routine products, stronger controls over data sharing and a clearer, auditable trail of consent.

Conclusion

CKYC has moved Indian onboarding from a repetitive, paper-heavy chore to a centralised, re-usable identity process. The user-centric benefits, reduced repetition, faster account opening and better privacy controls are being matched by systemic advantages for financial institutions and regulators.

With the upgraded CKYC registry and new technology implementations underway, the banking industry can expect smoother onboarding, improved compliance and better customer experience.

Firms that adopt CKYC-enabled flows and integrate robust CKYC APIs will be best placed to convert prospects quickly and securely. Take the first step now: contact Protean eGov Technologies for more information.

Frequently Asked Questions (FAQs)

- What is a CKYC number?

A CKYC number is a unique identifier issued when an individual’s KYC records are uploaded to the Central KYC Registry. It links to the customer’s validated KYC dossier and can be quoted for future financial relationships.

- Is CKYC mandatory in India?

CKYC is mandatory for certain types of financial relationships and is the accepted standard for KYC in many regulated entities. Where CKYC exists, quoting a CKYC number simplifies compliance for both customers and the institution.

- How do I get my CKYC number?

You obtain a CKYC number when you complete KYC with any registered financial entity that uploads your details to the central registry. Institutions will provide or display the CKYC number, and customers can request it if required.

- How can I update my CKYC details?

Updates to KYC, such as address changes are typically submitted through the financial entity where you hold an account. The entity updates your record in the CKYC registry, which then propagates the validated change to authorised users of the registry. Official advisories and implementation notes from the CKYC registry should be followed for specific processes and timelines.

Related Articles